Already have a car you like?

You might be sitting on untapped tax savings.

Many employees assume savings only come from buying a new vehicle. That is not the case. If your car is eligible, there is a way to keep driving it while reducing your running costs through salary packaging.

This is where a sale and leaseback comes in.

The Problem With Owning a Car Outright

Owning a car outright feels simple. No repayments. No finance. No paperwork.

But there is a downside most people overlook.

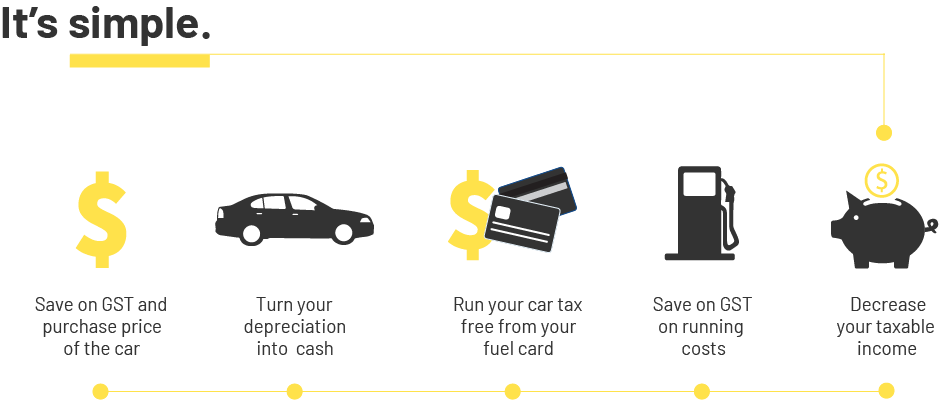

All you car costs are paid from after-tax income (fuel, servicing, insurance, registration, and tyres). It all adds up, and you are paying for it with money that has already been taxed.

For many employees, that means missing out on savings that are already available to them.

What is a Seal and Leaseback?

A sale and leaseback allows you to salary package your existing car instead of buying a new one.

In simple terms, your current vehicle is purchased at market value and then leased back to you under a novated lease arrangement. You continue driving the same car, but it is now packaged through your salary.

Nothing changes day to day. Same car. Same keys. Same routine.

What changes is how the costs are paid.

How It Works Step By Step

The process is more straightforward than most people expect.

First, your current car is assessed to confirm it meets eligibility criteria. This includes age, condition, and remaining value.

Once approved:

- The car is valued at its current market price

- That value is paid out, which can clear existing finance or go to you

- A lease is set up using that value

- Your car expenses are bundled into regular salary deductions

From there, running costs are paid from a mix of pre-tax and post-tax income, depending on your situation.

Why This Can Lead to Real Savings

The key benefit is how your car expenses are treated.

Instead of paying for everything from after-tax income, many costs can be packaged from your salary before tax. This reduces your taxable income and can lower your take-home cost of owning the car.

Typical expenses that can be included are:

- Fuel or charging

- Servicing and maintenance

- Registration

- Insurance

- Tyres and roadside assistance

Over time, this can make a noticeable different to your weekly budget.

Who a Sale & Leaseback Suits Best

A sale & leaseback works well for people who:

- Own their car outright or are close to paying it off

- Like their current car and do not want to change

- Want to reduce running costs without upgrading

- Are eligible to salary package through their employer

It is also popular with employees who recently purchased a car privately and later realised they could have packaged it.

Person handing over car keys.

What Happens If There Is Existing Finance?

If your car still has finance attached, that does not automatically rule it out.

In many cases, the sale component can be used to pay out the existing loan. Any remaining balance is then structured into the lease.

Each situation is different, which is why it is important to review the numbers before proceeding.

Things To Keep In Mind

A sale & leaseback is not suitable for every car or every employee.

Age limits, condition requirements, and employer policy all play a role. The best outcomes come from understanding:

- Your remaining car value

- How long you plan to keep the vehicle

- Your income and tax position

This is not about pushing a product. It is about checking whether the structure actually works for you.

Turning What You Already Own into Smarter Savings

Buying a new car is not the only way to improve your car finances.

If you already own a vehicle, a sale and leaseback can be a practical way to unlock savings without changing what you drive. The car stays the same. The structure improves.

Sometimes the smartest move is not upgrading. It is optimising what you already have.

Ready to see if your car is eligible?

A quick assessment can confirm whether a sale and leaseback suits your situation and what the potential savings look like.

If you want to understand how your current car could work harder for you, it starts with a simple conversation.